Graph(s) of the week: Companies' cash holdings

According to numerous reports, it seems that the biggest world companies are sitting on record levels of cash holdings. If this is true, the question is why aren't they spending it?

According to Financial Times, in 2008 the biggest 1000 world companies held a total of $1.95tn in cash, however by the end of 2012 this level has jumped up to $3.2tn. This can be attributed solely to the credit slump and the consequential severe lack of confidence during the entire recovery period.

However in 2013 the cash reserves kept on rising despite a rebound in the stock market and rising business confidence with still very low interest rates. All this should have encouraged more spending and investing from the business side, but cash reserves just kept on rising.

|

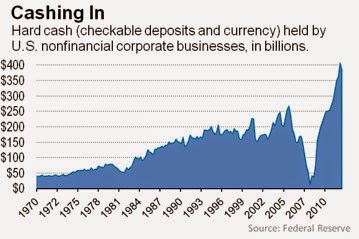

| Source: WSJ and US Federal Reserve |

|

| Source: The Telegraph |

However, it is obvious the distribution of these funds are uneven. The very fact that only the top companies are holding all this cash is biasing the estimate. The top 10 companies (Apple, Microsoft, Google, Verizon, Pfizer, Cisco, Oracle, Johnson&Johnson, GM and Intel) account for more than 10% of the total amount. The FT reports that companies with more than $2.5bn in cash holdings (really big companies) account for 82% of the total amount.

On the other hand many smaller and medium-sized companies are in lack of proper funding, and have maintained this position ever since 2008. Companies outside the top 1000 are taking more debt as they are taking advantage of low interest rates and cheep borrowing. So there are basically two divergent scenarios; one for highly profitable firms which hardly face any financing issues but are still holding on to their cash, and the second for small and medium companies which, as always, lack funding and have to rely on loans.

"Fiscal policy affects cash holdings in two ways, both of which involve taxes. First, public firms are seeing their profits rise elsewhere in the world; if these firms were to bring these profits from overseas operations back to the U.S., the profits would be relatively heavily taxed. Second, uncertainty about future taxes is on the rise.

Other explanations point to gradual changes in the nature of the operations of a firm. The leading hypothesis in this group relates the rise in cash holdings of U.S. corporations to the increasing predominance of research and development (R&D). Since R&D is an activity intrinsically connected with uncertainty, the association of R&D and cash holdings is a natural one. The rising importance of R&D in the overall economy is a long-term phenomenon that is due to the rapid growth of information technology firms."

The R&D hypothesis is a much more likely explanation in case of IT companies, whereas the tax uncertainty story relates more to other multinationals. So when should we expect a reversal of the trend? In terms of fiscal policy an approach designed at balancing the budget would definitely lower the tax uncertainty, but as for the R&D story this may well last for the next several years.

Comments

Post a Comment