Hits and misses: Evaluating last year's predictions

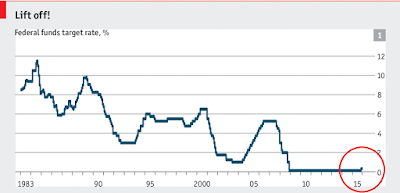

This is becoming a sort of a post-Christmas tradition on the blog - each year in the weak after Christmas I offer a wrap up of the year by evaluating my last year's predictions . Once again, I have to say, it was a good year in terms of what I got right (I managed to even beat my own predictions from 2014 : 85% compared to last year's 75%), but there were a few events that went under my radar (the Greece situation triggered by Syriza's victory, and the refugee crisis). The title of last year's predictions was: "2015: Back to Realpolitik and back to growth" . My main prediction was that most economies in the West would return to having steady rates of economic growth (which came true), and that debates over the economy will be overshadowed by the return of realpolitik and muscle-flexing between Russia and the West. I've also stated that "low oil prices will be the key in prompting a stronger recovery", which they were, and I managed to exclu...